Cash is king: why I'd rather grow slower than give up control

This is the fifth post in a series of five, excerpted from lessons in business by our founder, Peter Gradwell. They are taken from a YouTube interview he did in the "UK Business Forums" podcast series.

By 2006 or 2007, Gradwell had outgrown its infrastructure. We needed a proper cluster, not fourteen servers Sellotaped together, and the quote from HP came in at roughly $2 million. We didn't have $2 million. So off we went to NatWest Bank — my bank since I was 18 — to ask nicely for a loan.

The conversation was short. You're a fast-growth technology company with no balance sheet, we can't lend to you. Also — they didn't say this bit, but it was true — NatWest at the time was recovering from its own problems and had no money to lend. What you need, they said, is venture capital.

So we raised venture capital: a million pounds from Altitude Partners after about nine months of work, lawyers, due diligence, and thirty percent of the company handed over.

Then I went back to HP with my chequebook. HP said: put that away, Mr Gradwell. Our internal bank, HP Bank of Ireland, will lend you the two million dollars over five years at 1% interest on an asset-finance basis.

I said: why didn't you do that last week? They said: last week you weren't bankable. This week you have venture-capital backing. You're a good credit risk now.

"The more self-sustaining you can make your business, then as the entrepreneur, the more you're in control of it."

I ended that week two million dollars in asset-financed debt and having given away thirty percent of my company to raise a million pounds I didn't strictly need. The business hadn't changed between Monday and Friday. What had changed was the perception of the business — by the same banks and vendors who'd turned us away days earlier.

What I'd do differently

Two things, knowing what I know now:

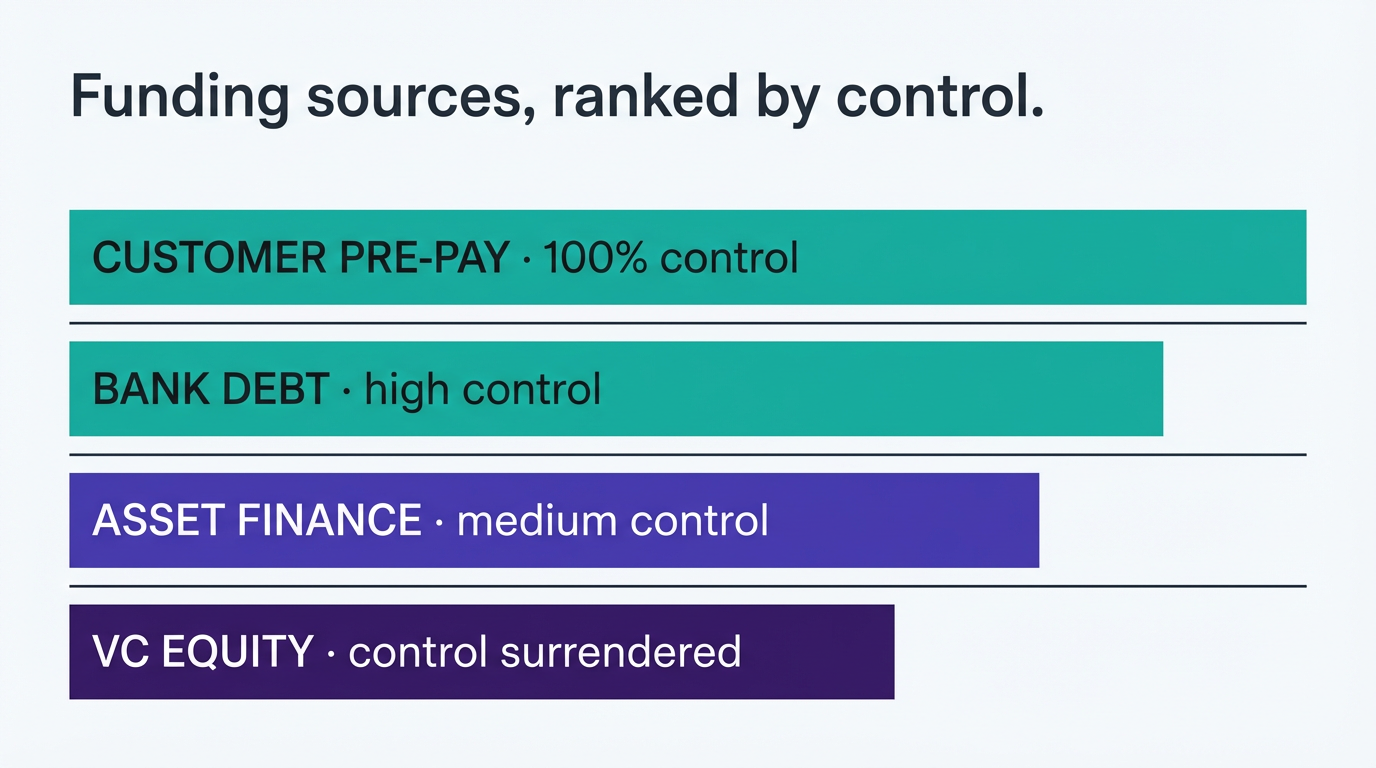

- Exhaust bank and asset finance before equity. Debt is expensive in money but cheap in control. Equity is the opposite. The order matters: supplier credit, customer pre-payment, asset finance, bank debt, then equity. Most founders run the ladder in reverse.

- Charge customers up front where you can. Annual billing instead of monthly. Twelve-month terms with a discount. Deposits on complex installs. This is the cheapest working capital you'll ever raise and it comes without covenants or board seats.

The self-reinforcing loop

The most interesting pattern in the HP story isn't about HP. It's that once you have a credible cap table, credit opens up everywhere — supplier terms get longer, asset finance becomes available, leases get signed, even recruiters will take you on retained terms. The single event of raising equity unlocks a dozen non-equity financing options that you could, in principle, have used without raising equity at all.

Which means the equity round you needed in order to unlock those options was often a round you didn't actually need. You needed the perception of being backed; you didn't need the money.

Cash is king — and it doesn't matter how profitable the business looks on paper. As soon as cash runs out, the business is gone. The corollary is: the more you can run the business on its own cash, the longer you get to keep driving it. Equity accelerates growth. Debt accelerates growth. Customer pre-payment accelerates growth and keeps you in the driver's seat. Of the three, only one lets you make your own mistakes on your own timeline.

That's what "control" really means. Not being a dictator. Just being able to decide, in a tough quarter, whether the right answer is to cut, to hold, or to double down — without three other people at the table whose incentives aren't quite your incentives.

Grow organically for as long as you possibly can. When you finally have to raise, raise on your own terms. And remember that the cheapest capital you'll ever deploy is the capital your customers send you, in advance, because they trust you to deliver.